The stablecoin market has crossed $250 billion in 2026. That number doesn’t happen by accident, it reflects years of crypto users discovering that not every digital asset needs to be volatile. For anyone trading crypto, sending money across borders, or just trying to hold value without watching it collapse overnight, a stablecoin is the infrastructure that makes it possible.

This guide covers everything that matters: what a stablecoin is, how stablecoins work mechanically, the main types you’ll encounter, a direct tether vs usdc comparison, and what the 2026 regulatory wave actually changed for users.

A stablecoin is a cryptocurrency designed to hold a fixed value, typically $1, by backing each token with reserves, collateral, or algorithmic controls. For most users, USDT works best for active trading, USDC for long-term holds, and regulated activity.

What Is a Stablecoin?

Stablecoins collectively hold over $250 billion in market cap in 2026, and move more than $2 trillion in monthly volume, surpassing PayPal’s annual transaction throughput (DeFiLlama, 2026). In practice, a stablecoin is a blockchain token that tracks the dollar, built to combine the speed and accessibility of crypto with the price predictability of traditional currency.

Luis Ferreira, Commercial Director VASP at Bank of London, frames the shift: the GENIUS Act gives stablecoins “recognition as the link between traditional finance and digital assets,” with transparency requirements that “build trust with banks and retailers.”

A stablecoin is digital cash. Wire it anywhere, it arrives in minutes. Hold it without watching the value halve overnight. And unlike a bank transfer, it works at 2am on a Sunday.

That last point is what distinguishes stablecoins from everything else in crypto. Where Bitcoin’s price floats freely with supply and demand, a stablecoin has a specific mechanism built to keep it exactly at $1. The mechanism varies by type, and the differences matter.

I started using USDC as a staging area between trades. Instead of converting back to fiat and losing two days to a bank wire, I’d park profits in a stablecoin and redeploy when the next setup appeared. No transfer fees, no settlement delays, no wondering if the wire would clear in time. It’s obvious in hindsight, but it changes how you think about moving in and out of positions.

How Do Stablecoins Work?

The most widely used stablecoins, USDT and USDC, maintain their $1 peg through direct reserve backing: for every token in circulation, the issuer holds $1 in reserves (Tether Holdings / Circle, 2025). Send $1 to the issuer, they mint one token. Redeem the token, they burn it and send your dollar back.

That minting-and-redemption loop is what keeps the price anchored. If USDT ever drifted above $1.00, arbitrageurs would mint new tokens cheaply and sell them back to parity. If it fell below $1.00, traders would buy cheap and redeem for the full dollar. The profit incentive pulls the peg back automatically, no issuer intervention required.

Reserve quality varies significantly between issuers. Circle (USDC) publishes monthly attestations verified by independent auditors, with reserves held in cash and a BlackRock-managed US Treasury money market fund. Tether (USDT) publishes quarterly reports, but its reserve composition has historically been less specific, a distinction that matters when assessing counterparty risk.

For anyone learning how stablecoins work for the first time: the reserve quality backstop is what separates a reliable stablecoin from one that could break its peg under pressure.

“The stablecoin market isn’t really about technology anymore — it’s about reserve management. The issuers who survive the next decade will be the ones who operate like narrow banks: full reserves, instant redemption, zero maturity mismatch. Everything else is a liability waiting to be tested.” — Jeremy Allaire, CEO of Circle

What Are the Main Types of Stablecoins?

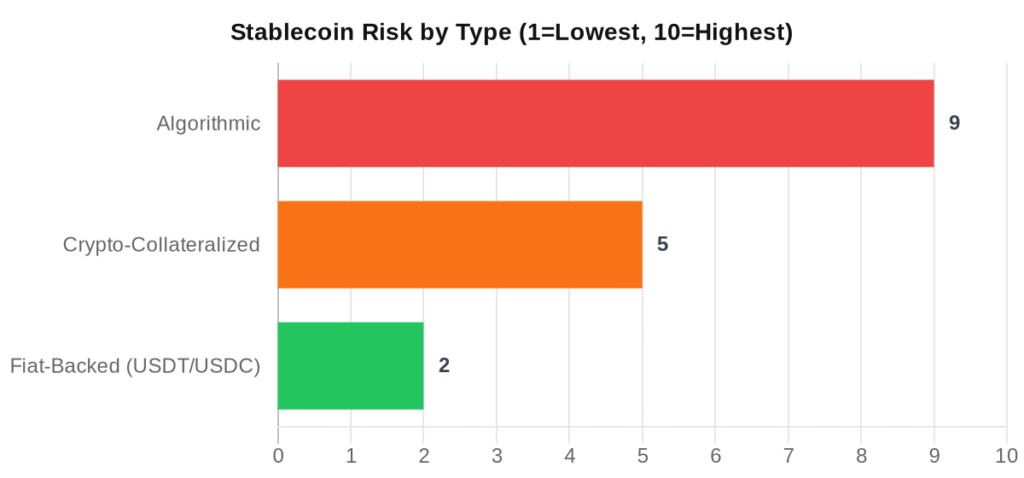

The mechanics differ significantly, and so do the risks. Fiat-backed stablecoins are the most tested at scale. Crypto-collateralized ones are more decentralized. Algorithmic stablecoins are the most experimental, and have the worst track record by far.

Fiat-Backed Stablecoins

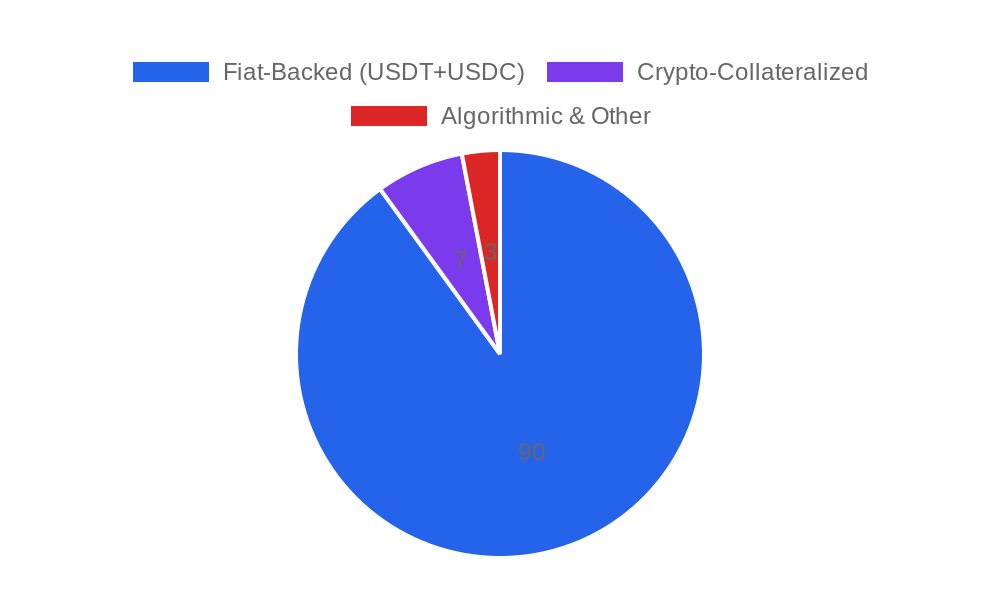

Fiat-backed stablecoins hold real cash or equivalent assets in custody, one token equals one dollar in reserve. They’re the dominant model, representing roughly 90% of total stablecoin market cap (DeFiLlama, 2026). USDT and USDC are the two most important examples; PayPal’s PYUSD is a newer entrant from a traditional finance giant.

The main risk is counterparty risk. You’re trusting the issuer to hold the reserves they claim. Circle’s monthly attestations give USDC a meaningful transparency edge, there’s a documented, audited paper trail. Tether holds reserves, but its history of opacity is a known issue; the US Commodity Futures Trading Commission fined Tether $41 million in 2021 for misleading statements about its reserve composition (CFTC, 2021).

Crypto-Collateralized Stablecoins

Rather than holding dollars in a bank, these stablecoins lock up cryptocurrency as collateral, more than $1 of collateral per $1 issued. DAI (now USDS, issued by Sky Protocol) works this way: lock ETH in a smart contract, and the protocol mints DAI against that position.

Overcollateralization is the buffer against volatility. If ETH drops, smart contracts automatically liquidate undercollateralized positions before the collateral value falls below the stablecoin value. It’s transparent and runs without a central issuer, which is the appeal for DeFi users.

The downside: capital inefficiency. You lock $1.50 to borrow $1. And if collateral prices crash fast, liquidation mechanisms can fail. That’s exactly what happened during the March 2020 “Black Thursday” crypto crash, when Ethereum’s price dropped 30% in hours and some DAI vaults went undercollateralized before liquidation bots could act.

Algorithmic Stablecoins

This is where things get complicated. And expensive, if you’ve lived through one of the failures.

Algorithmic stablecoins try to maintain their peg through supply mechanics rather than reserves, automatically expanding or contracting the token supply to keep the price at $1. No backing required. The concept is elegant. The execution has repeatedly failed at scale.

The defining disaster was TerraUST (UST) in May 2022. UST maintained its peg through a two-token model: UST as the stablecoin, LUNA as the reserve-like mechanism. When coordinated selling started, the feedback loop ran hot, UST fell, LUNA was minted to defend the peg, LUNA’s price crashed from selling pressure, which made UST fall further. In seven days, over $45 billion in market value was wiped out (CoinGecko, 2022). Not from a hack or fraud, from the architectural design failing exactly as critics had warned.

The 2026 GENIUS Act and MiCA in Europe effectively removed algorithmic stablecoins from the regulated category. They cannot be marketed as “stablecoins” under most major frameworks. Whether that ends the model or just moves it to less regulated venues is still playing out.

TerraUST wasn’t a scam. The team was technically sophisticated, the whitepaper was widely praised. The failure was structural, algorithmic models that rely on reflexive market mechanics have a failure mode that activates precisely when you need stability most. The GENIUS Act’s blanket exclusion of unbacked stablecoins isn’t overcorrection; it’s the lesson learned earlier.

Tether vs. USDC: Which Should You Use?

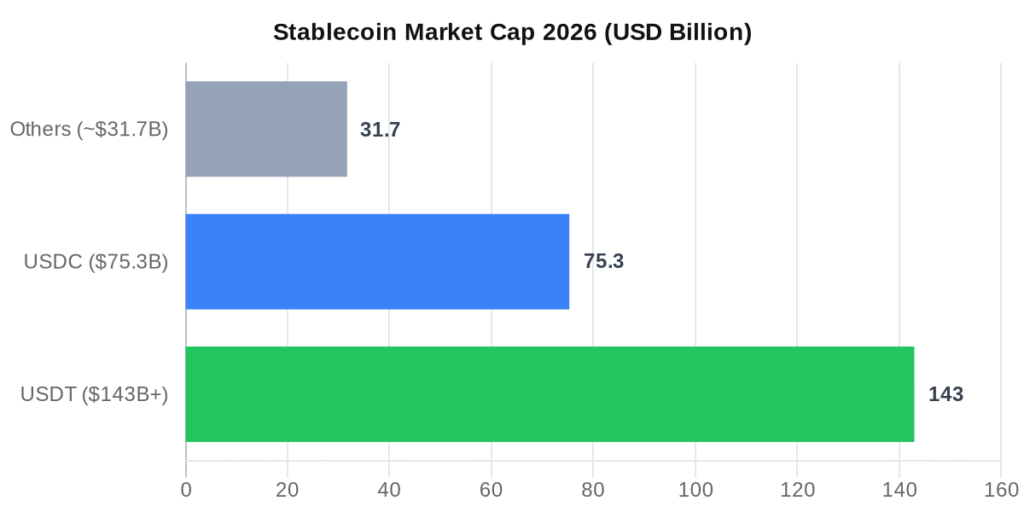

USDT and USDC together account for roughly 90% of all stablecoin market cap, with USDT at $143B+ and USDC at $75.3B and growing at 72% year-over-year (DeFiLlama, 2026). Understanding the tether vs usdc tradeoffs comes down to what you’re actually trying to do.

| Feature | USDT (Tether) | USDC (USD Coin) |

|---|---|---|

| Launched | 2014 | 2018 |

| Issuer | Tether Holdings | Circle |

| Market Cap (2026) | $143B+ | $75.3B |

| Reserve Audits | Quarterly (limited detail) | Monthly (full independent attestation) |

| Reserve Manager | Tether Holdings | BlackRock (via Circle Reserve Fund) |

| Regulatory History | $41M CFTC fine (2021) | Proactively compliant; MiCA-approved |

| Exchange Coverage | Virtually all major exchanges | Most major exchanges |

| Best For | Active trading, emerging market access | Long-term holds, institutional, regulated use |

The short version: USDT for trading liquidity, USDC if you’re holding serious sums and care about what’s behind it.

USDT still dominates global order books, deeper markets, more pairs, and a huge footprint in Southeast Asia and Latin America where dollar access through banking is limited. If you’re moving in and out of positions quickly, USDT’s liquidity advantage is real.

USDC is the better pick for capital preservation. Monthly attestations, BlackRock-managed reserves, and clean regulatory status make it the choice for long-term holders, corporate treasury, and anything that touches regulated financial infrastructure. USDC’s 72% year-over-year growth in 2026 reflects institutions voting with their capital.

What Are Stablecoins Used For?

Stablecoins process more than $2 trillion in monthly settlement volume, more than PayPal’s annual throughput and closing in on legacy rails like ACH (Chainalysis, 2026). The best stablecoin for a given use case depends on what you’re doing.

- Trading and DeFi is where most of the volume sits. Active crypto trading pairs against stablecoins rather than fiat, exiting a Bitcoin position without touching a bank means selling to USDT or USDC. DeFi lending protocols, liquidity pools, and yield products all run on stablecoin collateral. If you’re exploring crypto trading for beginners, stablecoins are the foundational concept you need to understand first.

- Cross-border remittances are the most direct real-world use case. Sending $500 from the US to the Philippines traditionally took 3–5 days and cost 6–8% in fees. A stablecoin transfer settles in minutes and costs cents. In countries where local currencies are losing value rapidly, Nigeria, Argentina, Venezuela, stablecoins have become a practical alternative to bank accounts.

- Corporate treasury is growing quietly. Companies holding crypto increasingly park their “safe” allocation in stablecoins rather than converting to bank cash. Instant deployment, 24/7 liquidity, no custody friction. Some treasurers now use stablecoin holdings to earn yield on short-term idle capital through DeFi, though that adds smart contract risk back in.

Everyday payments remain early. Visa and Mastercard both support USDC settlement networks. Some payroll providers offer stablecoin payroll. It’s not mainstream, yet, but the infrastructure is being built now.

Are Stablecoins Safe? Risks You Should Know

Fiat-backed stablecoins from reputable issuers are among the lowest-risk crypto assets. That’s a meaningful statement. Not risk-free, specific risks are real and worth understanding, particularly if you’re new to fundamental analysis for crypto.

- De-pegging risk: Even USDT briefly traded at $0.95 during the 2022 market contagion. It recovered, but holders who sold in a panic took real losses. The better-reserved a stablecoin is, the faster it historically recovers. The risk of a complete, permanent loss from USDC or USDT de-pegging is low. Algorithmic stablecoins? History suggests otherwise.

- Counterparty risk: When you hold USDC, you’re trusting Circle to maintain full 1:1 reserves. Circle is regulated, publishes monthly attestations, and holds reserves in a BlackRock government money market fund, that’s a serious institutional credibility layer. Tether’s reserve opacity is documented history; the CFTC’s $41 million fine for misleading reserve statements is on the public record. Both are functional, but the risk profile is different.

- Smart contract risk: For crypto-collateralized and algorithmic stablecoins, a bug in the on-chain mechanism can drain funds or break the peg without any human intervention. DAI has run for years without a critical exploit, but the theoretical risk exists in any smart contract system. The history of blockchain is littered with smart contract vulnerabilities that cost users real money.

- Regulatory risk: In 2026, the direction is toward more regulation of compliant stablecoins, which actually reduces risk for USDC and USDT holders. But for algorithmic or yield-bearing stablecoins, the GENIUS Act and MiCA have effectively pushed them outside regulated markets.

The TerraUST case defines how badly algorithmic failures can go. In May 2022, the two-token UST/LUNA architecture failed under selling pressure. The feedback loop was built into the design: UST fell, LUNA was minted to defend the peg, LUNA selling crashed its price, which accelerated UST’s decline. $45 billion disappeared in one week (CoinGecko, 2022). Investors who assumed “stablecoin” meant “safe” learned the opposite. The lesson: the label matters far less than the backing.

Stablecoin Regulation in 2026: What Actually Changed?

Stablecoin regulation moved from theoretical to mandatory in 2025–2026. Seven major economies, US, EU, UK, Singapore, Hong Kong, UAE, and Japan, now have or are finalizing stablecoin-specific frameworks requiring reserve backing, licensed issuers, and redemption rights.

In July 2025, President Trump signed the GENIUS Act into law, the first comprehensive federal framework for payment stablecoins in the US. The OCC issued proposed implementing rules in February 2026. Every regulated stablecoin must hold 1:1 dollar reserves in high-quality liquid assets, issuers must be licensed, and holders must have guaranteed redemption rights. Algorithmic and yield-bearing stablecoins are excluded from the regulated category.

In Europe, MiCA (Markets in Crypto-Assets), which took full effect in 2024, applies similar logic. Fiat-backed stablecoins must hold 1:1 reserves in segregated bank accounts or government bonds. Circle achieved MiCA compliance in 2024. Tether secured EU compliance in late 2025.

For users, the practical effect is mostly positive: the regulated stablecoins are getting stronger institutional infrastructure underneath them. Banks, brokers, and payment processors are more willing to integrate stablecoins now that regulatory status is defined. For users of algorithmic or unregistered stablecoins, the picture is different, access to regulated markets is narrowing.

Where this goes next is genuinely open. The future of blockchain and digital currency includes CBDCs (central bank digital currencies) that could compete directly with stablecoins in some use cases. That’s a longer-term conversation.

The Bottom Line on Stablecoins

A stablecoin is a cryptocurrency pegged 1:1 to the dollar that exists to give crypto users the benefits of blockchain infrastructure without the volatility. Stablecoins are the functional backbone of the crypto economy, the settlement layer that everything else runs on.

So what should you actually do? If you’re an active crypto trader, you’re almost certainly already using stablecoins, USDT dominates exchange order books and is the practical default. If you’re new to crypto and want to hold digital assets without price risk, USDC is the better starting point: transparent reserves, regulated issuer, BlackRock-managed backing. And avoid algorithmic stablecoins until you fully understand the mechanics. It was the architecture behaving exactly as it was designed, in the worst possible conditions.

For a broader view of how stablecoins fit into the digital asset ecosystem, explore our guide to the types of cryptocurrency.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice, always do your own research and consult a qualified advisor before buying, holding, or transacting in any stablecoin or crypto asset.

Frequently Asked Questions

1. Is a stablecoin the same as real money?

No. It’s a blockchain token, not government-issued legal tender. The issuer (Circle for USDC, Tether Holdings for USDT) holds the reserves, not a central bank. What you hold is a claim on those reserves, redeemable 1:1 for a dollar.

2. Can I earn interest on stablecoins?

Yes, through DeFi protocols, centralized exchanges, and some licensed platforms. Rates range from 1–2% on conservative options to higher yields in DeFi liquidity pools. Under the GENIUS Act, US-regulated stablecoins themselves cannot carry embedded yield, but yield products built on top of stablecoins remain available. Understand the risk profile of wherever you’re depositing.

3. What’s the best stablecoin to hold in 2026?

USDC from Circle for most users. Monthly attestations, BlackRock-managed reserves in a government money market fund, MiCA compliance, and clean regulatory history make it the safest option by reserve quality. USDT remains better for active trading due to deeper exchange liquidity. For a broader view of the crypto asset landscape, see our guide to the future of cryptocurrency.

4. What happened to TerraUST?

TerraUST (UST) was an algorithmic stablecoin that used a companion token, LUNA, to maintain its $1 peg. In May 2022, a large coordinated sell-off triggered a death spiral: UST fell, LUNA was minted to defend the peg, LUNA crashed from the selling pressure, which made UST fall further. Over $45 billion in market value was erased in a week. The GENIUS Act now effectively bars algorithmic stablecoins from the regulated market.

5. What is the difference between USDT and USDC?

Both are fiat-backed stablecoins pegged 1:1 to the US dollar. USDT (Tether, launched 2014) has the larger market cap and deeper trading liquidity, better for active trading. USDC (Circle, launched 2018) has stronger reserve transparency, full monthly attestations, and regulatory compliance across major jurisdictions, better for long-term holding and institutional or regulated use cases.

Our Review Methodology

We evaluate each post based on thorough research, credibility of sources, accuracy of information, and relevance to our readers. Our editorial team follows strict guidelines to ensure all content meets high standards of quality.

Disclaimer

The content in this article is provided for informational purposes only and does not constitute financial, investment, or professional advice. Always do your own research before making any decisions.