If you’ve tried to sign up for a crypto exchange recently, you’ve almost certainly hit a wall of identity checks before you could deposit a single dollar. That’s KYC — Know Your Customer — and it’s not going anywhere. In fact, it’s getting stricter.

This guide covers what KYC actually means on a crypto exchange, why exchanges are legally required to collect your details, what the process looks like step by step, and what happens if you’d rather not hand over your passport.

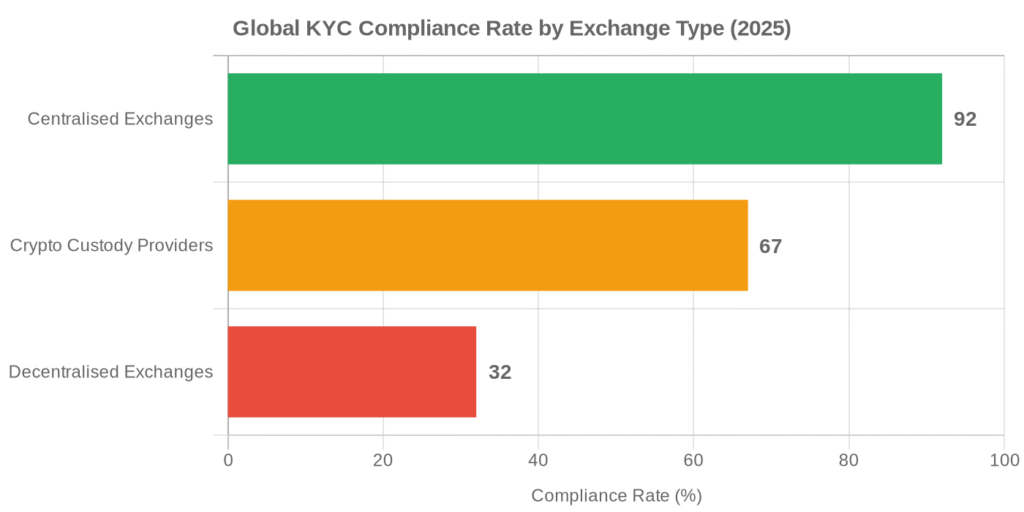

KYC (Know Your Customer) is the process of identity verification which crypto exchanges use to comply with anti-money laundering laws. You’ll need a government ID, proof of address, and sometimes a selfie. As of 2025, 92% of centralised exchanges require it (CoinLaw.io, 2025). Skipping it limits your withdrawal access and may get your account suspended. DEXs and some peer-to-peer platforms still allow trading without full verification — with real trade-offs.

What Does KYC Actually Mean in Crypto?

KYC stands for Know Your Customer — identity verification procedures that financial institutions use to confirm who they’re doing business with. In crypto, this means the exchange needs to verify that you are who you say you are before letting you trade, withdraw, or move money.

It’s not a crypto-specific invention. Banks have been doing it for decades. The Financial Action Task Force (FATF) — the global standards body for anti-money laundering — extended these requirements to virtual asset service providers (VASPs) in 2019, pulling crypto exchanges firmly into the same regulatory framework as traditional finance.

“FATF’s 2019 update to Recommendation 15 explicitly brought cryptocurrency exchanges under the same AML/KYC framework as conventional financial institutions,” the FATF noted in its guidance on virtual assets (FATF Virtual Assets Guidance, 2019). That shift triggered a wave of compliance rollouts across major exchanges globally.

From Banking to Blockchain: Why KYC Followed Crypto Here

Crypto’s early years had a reputation for being the wild west — anonymous transactions, no identity checks, genuine appeal for anyone who wanted to move value without oversight. Regulators noticed. Over 120 countries now require crypto exchanges to implement KYC compliance, and the holdouts are shrinking fast.

The original purpose was straightforward: if you know who your customers are, it’s harder for criminals to move dirty money through your platform. AML (anti-money laundering) and CTF (counter-terrorism financing) requirements are the legal architecture around that logic, and KYC is the front door.

Why Do Crypto Exchanges Require Identity Verification?

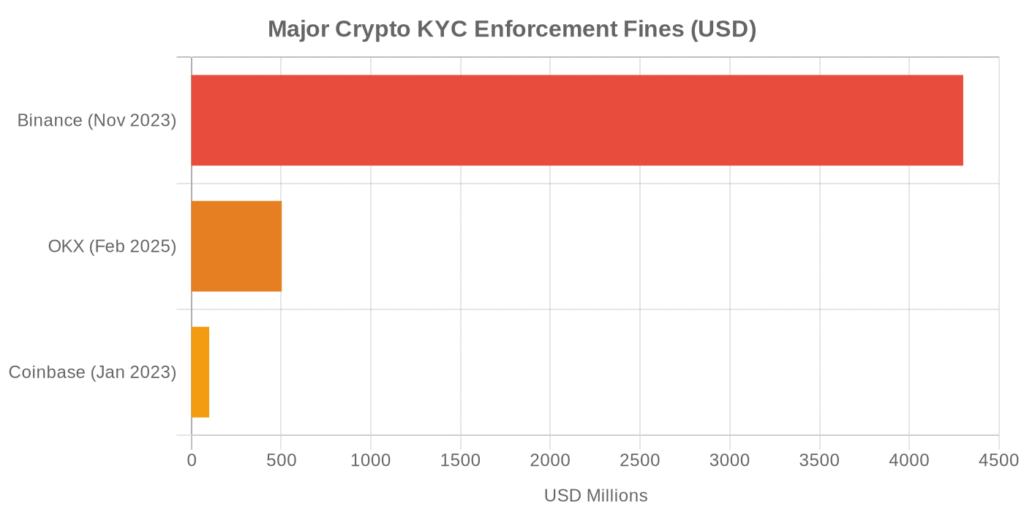

The blunt answer: because regulators will fine them into the ground if they don’t. In November 2023, Binance settled for $4.3 billion with the U.S. Department of Justice, FinCEN, and OFAC — the largest corporate criminal penalty in crypto history — after admitting it “willfully failed” to run adequate KYC on a large number of its users (U.S. Treasury, 2023).

And Binance wasn’t alone. In the first half of 2025 alone, regulators issued 139 fines totalling $1.23 billion for AML, KYC, and sanctions violations — a 417% increase in value compared to the same period in 2024 (CoinLaw.io, 2025). OKX paid $504 million to the DOJ in February 2025 after processing billions in suspicious transactions through inadequate identity controls.

Beyond the fines, there are real business reasons. Exchanges that pass KYC scrutiny can access banking rails, get listed on institutional platforms, and process fiat deposits and withdrawals. Those that don’t tend to find themselves cut off from the payment infrastructure that makes a crypto exchange actually useful.

It’s worth checking a platform’s Trust Score before depositing — it factors in regulatory status and KYC practices alongside fees and features when evaluating any exchange.

What Documents and Information Does a Crypto Exchange KYC Require?

Most centralised exchanges require three things: proof of who you are, proof of where you live, and a biometric check to confirm you’re not submitting stolen documents. The exact requirements vary by platform and jurisdiction, but the broad strokes are consistent enough that you can prepare in advance.

Individual Verification

For personal accounts, expect to provide:

- Government-issued photo ID — passport, national ID card, or driving licence. A photo is usually fine, though some platforms now use NFC chip reading (your phone tapping your passport) for higher-assurance verification.

- Proof of address — utility bill, bank statement, or official government correspondence, generally dated within three months. The address must match what you entered during registration.

- Selfie or liveness check — you’ll hold your ID next to your face, or complete a short video liveness test. AI systems check simultaneously that you’re a live person (not a printed photo), that your face matches the document, and that the document itself appears authentic.

Some platforms run in tiers. Basic verification (name, email, date of birth) unlocks limited crypto-to-crypto trading. Full verification — ID plus address document — unlocks fiat deposits, higher withdrawal limits, and features like margin trading or staking. Coinbase Wallet, for instance, only enforces identity checks when you connect to its integrated fiat services, not for wallet-only use.

Business/Corporate Verification

For companies, KYC goes several layers deeper. Exchanges typically ask for corporate registration documents, proof of address for the business, and identity verification for all beneficial owners and directors (usually anyone with 25%+ ownership). Financial businesses must also submit AML policy documentation.

This is called KYB — Know Your Business — and it’s why setting up a corporate crypto account can take days or weeks rather than minutes. That’s roughly what you’d expect from any regulated financial service.

How Does the Crypto KYC Process Work, Step by Step?

Modern crypto KYC is faster than it used to be — when it works well, the whole process takes under five minutes, compared to 24-hour manual reviews that were standard just a few years ago (Prove.com, 2025).

- Step 1 — Registration. Create an account with email and password. At this stage you’re typically limited to browsing or very basic functions.

- Step 2 — Submit personal information. Full name, date of birth, nationality, residential address. Some platforms add phone number verification here before letting you proceed to document upload.

- Step 3 — Document upload. Photograph or scan your government ID. Most platforms accept a phone camera; some now offer NFC-based passport reading, which produces a higher-confidence result and tends to skip the manual review queue.

- Step 4 — Biometric liveness check. A selfie or short video confirms you match the document. The AI checks for facial geometry, document authenticity, and liveness simultaneously — the process that used to require a trained compliance officer now runs in seconds.

- Step 5 — Sanctions screening. Your details are checked against FATF watchlists, politically exposed person (PEP) databases, and OFAC/EU sanctions lists. This also runs in seconds in automated systems.

- Step 6 — Decision. Automated systems handle the clear majority of approvals instantly. Edge cases — blurry documents, name mismatches, or hits on screening databases — get flagged for human review, which can take anywhere from a few hours to two business days.

The frustrating part isn’t the technology. It’s the edge cases. If your name appears differently on your ID versus your utility bill, or your document is slightly expired, the automated system will kick it for manual review almost every time. Photographing your ID in good, even light (no shadows, no glare) eliminates most common rejection reasons before you even submit.

What Happens If You Don’t Complete KYC on a Crypto Exchange?

Abandoning KYC doesn’t delete your account — it limits what you can do with it. Most exchanges apply tiered restrictions to unverified users rather than shutting them out entirely, at least initially.

Typical restrictions on unverified accounts:

- Withdrawal caps — daily limits of roughly $500–$1,000 equivalent. On Binance, unverified users are limited to 0.06 BTC daily; MEXC allows up to approximately $1,000 without verification in most regions.

- No fiat access — you can’t deposit or withdraw in regular currency (dollars, euros, etc.) without identity verification.

- Feature lockouts — margin trading, staking, P2P trading, and higher-tier products are typically gated behind full verification.

- Risk of account suspension — if high-value transactions are detected on an unverified account, most platforms will freeze it until verification is completed.

The trajectory is clear. Several exchanges that previously allowed more anonymous trading have since introduced retroactive KYC requirements. Users who ignored earlier prompts found their accounts frozen mid-trade. There’s also a practical issue: without KYC, you lose the account recovery pathway. No proof of identity means support has no way to verify ownership.

Is There a Crypto Exchange Without Full KYC Requirements?

There are options — though “no-KYC” is getting harder to define, and the list of genuinely anonymous alternatives keeps shrinking. As of 2025, only 32% of decentralised exchanges (DEXs) implement even voluntary KYC measures (CoinLaw.io, 2025).

The main options for reduced-KYC trading:

- Decentralised exchanges (DEXs) — platforms like Uniswap, PancakeSwap, or dYdX let you connect a self-custody wallet and trade directly from it. No account creation, no identity checks. The trade-off is real: DEXs are crypto-to-crypto only, no fiat on/off-ramp. If you want to use actual currency to buy in, you still need a KYC-compliant exchange as your starting point.

- Peer-to-peer (P2P) platforms — services like Bisq run buyer-seller matching without a central custodian. You deal directly with another person and coordinate payment outside the platform. Lower limits, more friction, higher counterparty risk — but no mandatory KYC in most cases.

- Centralised exchanges with tiered KYC — some platforms allow basic withdrawals without full verification. These are low-KYC, not no-KYC, and the thresholds are tightening as regulation rolls out.

Worth being clear about one thing: using non-KYC platforms to avoid tax reporting obligations or hide regulated financial activity is not a legal grey area — it’s simply illegal in most jurisdictions. The appeal of financial privacy is legitimate and widely held. Using it as cover for evasion is a different matter entirely.

For a full comparison of what exchange types actually offer, our centralised vs decentralised exchanges guide covers the practical trade-offs including liquidity, fees, and custody models.

Is Crypto KYC Safe? What Exchanges Do With Your Personal Data

This is where exchanges have, frankly, a mixed record. The requirement to collect identity documents is legally non-negotiable, but how well exchanges protect that data once collected is an entirely separate question.

In 2024, a breach affecting Gemini users exposed personal data, including names, email addresses, and partial financial details. More recently, a 2025 Coinbase security incident compromised customer KYC records — including ID scans — affecting a significant number of users. Neither breach resulted in funds being stolen directly, but exposed KYC data creates risks that outlast the incident: targeted phishing, SIM swapping, and identity fraud using your actual passport scan. I believe this is exactly the situation that gives rise to the question about bulk data security in exchanges.

What reputable exchanges should be doing (and what you should check for before handing over your documents):

- Document encryption at rest — your ID scan shouldn’t be stored as a plain file

- Data minimisation — collecting only what regulations require, not more

- Clear retention policy — how long are your documents kept after verification?

- Published breach response procedures — have they been tested?

None of this means you shouldn’t complete KYC on a trusted exchange. It means you should be thoughtful about which exchanges you hand your passport to. We evaluate security and KYC data practices in our crypto exchange reviews.

Once you’re verified and holding assets, it’s also worth thinking about where those assets live. Our guide on the safest way to store your crypto covers self-custody options that reduce your exposure if an exchange platform is ever compromised.

KYC Is Tightening in 2026 — What Crypto Traders Need to Know

Starting in 2026, U.S.-based crypto exchanges are required to issue Form 1099-DA — a capital gains and losses report filed with the IRS. To issue this form, an exchange needs to know who you are. That means any U.S.-accessible platform that hasn’t enforced full KYC has a hard regulatory deadline now.

The EU’s MiCA framework (Markets in Crypto-Assets Regulation) reached full implementation in December 2024, requiring all crypto asset service providers operating in the EU to maintain KYC-compliant onboarding. This isn’t a voluntary standard or a phased suggestion — it’s the legal baseline for operating in the EU market.

The practical upshot: even platforms that previously sat in regulatory grey areas are now cleaning up their user bases. If you’ve been trading on an exchange with light-touch identity checks, expect more verification prompts. I believe it is better to complete them proactively than have an account restricted mid-trade when you actually need access to your funds.

The Bottom Line on KYC for Crypto Exchanges

KYC on a crypto exchange is identity verification — legally required, increasingly automated, and getting harder to avoid as the 2026 regulatory wave locks in. For most users on reputable centralised platforms, the process takes under five minutes and unlocks full account access including fiat trading. The alternatives — DEXs, P2P platforms — are real but come with genuine limitations on fiat access, liquidity, and account recovery.

Before signing up with any exchange, check how they handle KYC data, what their compliance track record looks like, and whether they’ve experienced breaches. Our guide to the best crypto exchanges covers all of this, including which platforms have the strongest security practices alongside competitive fees.

Frequently Asked Questions

1. What documents are required for crypto exchange KYC?

Most exchanges require a government-issued photo ID (passport, driving licence, or national ID card) and proof of address (utility bill or bank statement dated within three months). A selfie or liveness check is also standard. Business accounts additionally require corporate registration documents and identity verification for all beneficial owners.

2. How long does crypto KYC verification take?

Automated systems typically approve straightforward individual applications in under five minutes. Edge cases — blurry documents, name mismatches, or hits on sanctions screening databases — are flagged for manual review, which generally takes between a few hours and two business days. Photographing documents in good light reduces the likelihood of a manual flag.

3. Do decentralised exchanges (DEXs) require KYC?

Most DEXs don’t require KYC because users connect self-custody wallets directly rather than creating accounts. Only 32% of DEXs implement even voluntary KYC measures as of 2025. The trade-off: DEX trading is limited to crypto-to-crypto — you still need a KYC-compliant exchange to convert fiat currency into crypto.

4. Does crypto KYC verification ever expire?

It can. Exchanges periodically request updated documents if your ID expires, your account reaches higher transaction thresholds, or regulations change in your jurisdiction. Some platforms trigger routine re-verification checks every 12-24 months as a standard compliance measure.

5. Is it legal to use a no-KYC crypto exchange?

In most jurisdictions, using a platform that doesn’t require KYC isn’t illegal in itself. What matters is what you’re doing with it. Using non-KYC platforms specifically to evade tax reporting, conceal sanctioned activity, or launder funds is illegal. Privacy-motivated trading for legitimate purposes sits in a jurisdiction-dependent grey area — one that is narrowing as regulatory frameworks tighten globally.

6. Can I use a VPN to bypass KYC?

No. VPNs mask your IP address but not your identity. Regulated exchanges require government-issued ID and selfie verification regardless of your connection location. Using a VPN to misrepresent your jurisdiction also violates most exchanges’ terms of service and can result in permanent account suspension.

7. What happens to my data if the exchange shuts down?

It depends on how the exchange shuts down. In a regulated insolvency, user data typically transfers to a court-appointed administrator or acquiring entity and is retained under the same compliance obligations. In an abrupt closure or hack, there’s no guarantee — your KYC documents (passport scans, proof of address) may remain on compromised servers with no recourse. This is one reason to favor exchanges regulated in jurisdictions with strict data retention and breach notification laws (FCA, MAS, FINRA-adjacent entities).

Disclaimer: This article is for educational purposes only and does not constitute legal or financial advice. KYC and AML requirements vary by jurisdiction. Traders should familiarise themselves with the specific regulations applicable to their country of residence.

Our Review Methodology

We evaluate each post based on thorough research, credibility of sources, accuracy of information, and relevance to our readers. Our editorial team follows strict guidelines to ensure all content meets high standards of quality.

Disclaimer

The content in this article is provided for informational purposes only and does not constitute financial, investment, or professional advice. Always do your own research before making any decisions.