I remember the first time I tried crypto yield farming. It was 2021, DeFi Summer was already a year old, and I deposited USDC into a liquidity pool promising 40% APY. Three weeks later I withdrew with something like 32% — after gas fees, impermanent loss, and a token reward that had depreciated by half. The yield was real. The math just didn’t work out the way the interface implied.

That’s yield farming in a nutshell: the returns are there, but so are the mechanics that eat into them. Understanding both is how you avoid the mistakes most beginners make.

Yield farming means depositing crypto into DeFi protocols such as liquidity pools, lending markets, or staking vaults to earn rewards paid in tokens or fees. Returns range from 2% APY on stablecoins to 50%+ on newer, riskier protocols. The risks are real: impermanent loss, smart contract vulnerabilities, and token inflation can all reduce what you actually take home.

What Is Crypto Yield Farming?

Crypto Yield farming is the practice of putting idle crypto assets to work. You deposit assets into a DeFi protocol a lending market, a liquidity pool, or a staking vault and the protocol rewards you for providing that liquidity. Those rewards come as transaction fees, newly minted governance tokens, or interest payments from borrowers.

The “farming” name is apt. Like crop rotation, active yield farmers move capital between protocols to chase the best returns. Unlike a traditional savings account, the APY isn’t fixed it shifts with supply, demand, and token price. A pool offering 25% APY today might drop to 8% next week if it attracts enough capital.

DeFi’s total value locked sat around $120 billion heading into early 2026, then slipped to roughly $105 billion during a February market selloff a 12% drawdown that held up better than crypto prices overall (CoinDesk, February 2026). That’s a lot of capital chasing yield. Most of it concentrates in a handful of protocols.

Worth knowing before you deposit: yield farming isn’t passive the way ETH staking is. You’re actively managing positions, monitoring rewards, sometimes claiming and reinvesting manually. If that sounds like work, it is. The people who do well treat it like a part-time job, at least at first.

How Does Yield Farming Work?

Start with a liquidity pool. Two tokens get deposited in a ratio usually 50/50 say, ETH and USDC into an automated market maker (AMM) like Uniswap. Every time someone swaps ETH for USDC through that pool, they pay a small trading fee. That fee gets distributed to everyone who provided liquidity, proportional to their share.

When you deposit, here’s what you actually receive:

- LP tokens — a receipt representing your pool share. Uniswap V2 issues UNI-V2 tokens; Curve issues crv3pool tokens. These are your claim on the underlying assets.

- Trading fee revenue — your proportional slice of every swap routed through your pool.

- Protocol rewards — many protocols layer additional incentives on top. Curve adds CRV token emissions. Aave distributes AAVE tokens. These are the “bonus yields” that make headlines.

Some protocols let you stake those LP tokens in a separate “farm” contract to earn even more rewards. That’s double-layer yield farming and it’s where complexity (and risk) stacks up fast.

The math is straightforward. If a pool holds $10 million total and you contributed $100,000, you own a 1% stake. If the pool generates $2 million in trading fees over a year, your cut is $20,000, a 20% return before any protocol token rewards on top. In practice, fee revenue varies dramatically by pool activity, and the numbers shift daily.

Yield Farming vs. Staking: Which Should You Use?

These two terms get used interchangeably, which causes real confusion. They’re different products.

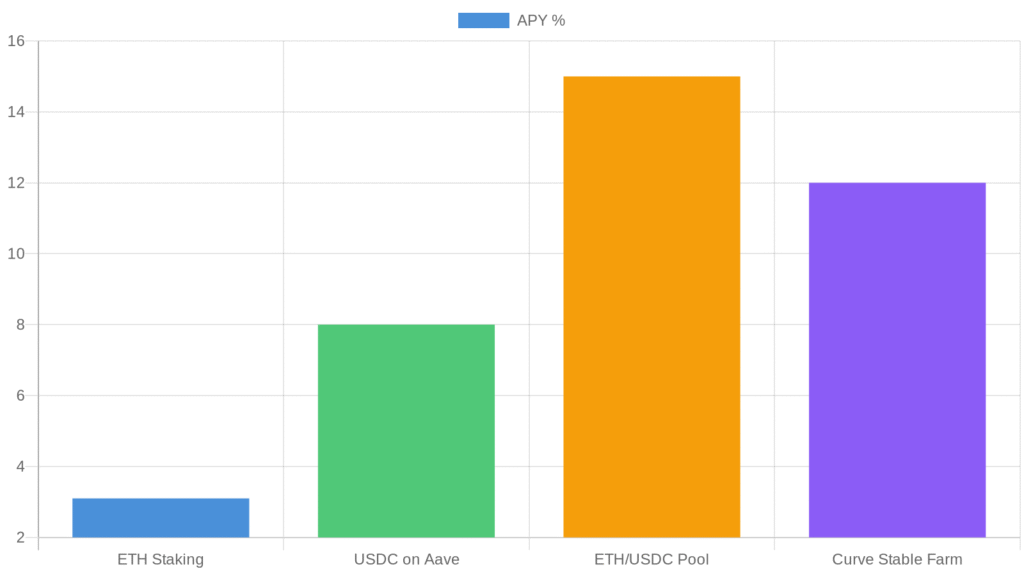

- Staking means locking tokens to help secure a proof-of-stake blockchain. Stake ETH through a validator, and you earn a cut of network issuance. As of early 2026, ETH staking yields around 3.1% APY (EarnPark, 2026). Predictable, relatively low-risk if you trust the network, but the upside is capped by protocol issuance rates.

- Yield farming targets higher returns at the cost of more exposure. Providing USDC to Aave was earning around 8% in early 2026, more than double ETH staking, for a stablecoin position that doesn’t fluctuate in price. Push into volatile pairs on a DEX and you find pools offering 30-80% APY, though those numbers compress quickly once capital floods in.

The honest side-by-side:

| Yield Farming | Staking | |

|---|---|---|

| Complexity | High, multiple steps, active management | Low, deposit and earn |

| Typical APY | 5-50%+ (varies widely by protocol) | 2-7% for major assets |

| Capital lock-up | Usually flexible, withdraw anytime | 7-21 days depending on chain |

| Primary risk | Impermanent loss, smart contract exploits | Slashing, network downturns |

| Best for | Stablecoins, active DeFi users | Long-term holders, passive income |

The short version: if you’re holding stables and want to put them to work, yield farming is worth understanding. If you’re a long-term ETH holder who doesn’t want to manage positions, staking is the cleaner path. Many experienced DeFi users do both, stake a core position for baseline yield, deploy a smaller allocation into farming for higher returns.

Best Yield Farming Platforms in 2026

Not all platforms are built the same.

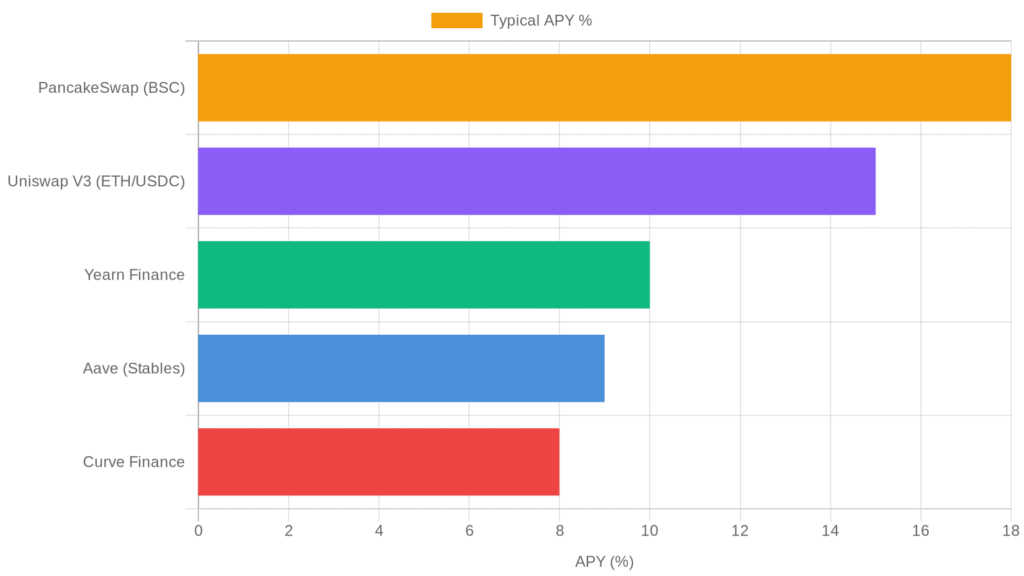

- Aave is the most established lending market in DeFi. Deposit USDC, USDT, DAI, ETH, or a handful of other assets and earn interest from borrowers. Yields range from 3% to 15% APY depending on asset and pool utilization. It’s been audited repeatedly and has survived multiple market crises without a major exploit at the protocol level. Good starting point for first-time yield farmers who want a lower-risk entry.

- Curve Finance is optimized for stablecoin liquidity. The fee model rewards providers differently than Uniswap: tighter pools, lower slippage, steadier fee revenue. The CRV token adds governance rewards on top. As of early 2026, Curve’s stablecoin pools typically yield 5-12% combined (fees plus CRV emissions), per DeFiLlama data. Fair warning: the Curve interface is notoriously confusing for new users.

- Uniswap V3 dominates AMM trading for volatile pairs. V3 introduced concentrated liquidity, you specify a price range where your capital is active. The upside: fee revenue is dramatically higher within that range. The catch: if the price moves outside your range, you earn nothing and may sit fully exposed to one asset.

- Yearn Finance automates the “which pool is best?” decision. Deposit USDC and Yearn’s vaults route it through whatever strategy currently produces the best return, rebalancing automatically. Less control, less management overhead. Yearn charges a performance fee of around 10-20% of yield, but the automation often more than compensates for hands-on management costs.

- PancakeSwap runs on Binance Smart Chain and offers significantly cheaper gas fees than Ethereum-based protocols, which matters when you’re compounding rewards manually. The trade-off is a less battle-tested ecosystem; BSC has seen more exploit incidents than Ethereum mainnet. Worth considering for smaller starting positions where Ethereum gas makes the math unworkable. If you prefer a centralized platform with DeFi-adjacent features, our OKX review covers its Earn product, which includes locked staking and DeFi farming access.

What Is Impermanent Loss And Why It Matters

Impermanent loss is the part yield farming guides often bury. It’s also the most common reason farming returns disappoint.

When you provide liquidity to an AMM, the pool automatically rebalances your token allocation as prices shift. If ETH doubles in price while you’re in an ETH/USDC pool, the pool sells your ETH and buys USDC constantly, algorithmically. By the time you withdraw, you hold less ETH than if you’d kept it in your wallet.

The math from a real example: you deposit 1 ETH (worth $3,000) and 3,000 USDC into a 50/50 pool. ETH rises to $12,000. When you withdraw, the pool’s rebalancing means you receive roughly 0.5 ETH and 6,000 USDC, worth $12,000 in total. If you’d just held, your 1 ETH alone would be worth $12,000 plus your 3,000 USDC: $15,000. The $3,000 difference is impermanent loss.

Volatile pairs suffer this significantly. Stablecoin pairs (USDC/USDT, USDC/DAI) have near-zero impermanent loss because the prices barely diverge. That’s exactly why stablecoin pools are the entry point most experienced DeFi educators recommend.

The “impermanent” label comes from the idea that if prices return to where they were at deposit, the loss evaporates. In practice, crypto prices don’t always return, making the loss very permanent for many farmers.

Other Risks You Can’t Ignore

Smart contract risk sits above impermanent loss on the danger scale. Every DeFi protocol runs on code. That code can contain bugs. When it does, attackers find them.

Harvest Finance suffered a multi-million dollar flash loan attack in 2020 — a reminder that protocols with substantial TVL can be drained in a single transaction (Chainalysis, 2023). Flash loan attacks don’t require the attacker to hold capital; they borrow, exploit, and repay within the same block. The attack vector has been replicated dozens of times across DeFi since.

A few more risks worth mapping before you deposit:

- Rug pulls — A new protocol launches with eye-catching APY, attracts capital, then the team withdraws liquidity and disappears. More common on BSC and smaller chains. Protocols without a public audit and an identified team are higher risk by default.

- Token inflation — Those governance token rewards boosting APY to 50%+? They’re freshly minted tokens. If there’s no sustained buying demand, the APY is partially illusory — you’re earning something that immediately loses value on the open market. Always check the token’s circulating supply growth rate before treating emissions as real yield.

- Gas fees — Ethereum gas fees make small positions economically unworkable. Claiming $40 in rewards when the transaction costs $25 in gas doesn’t make sense. This is less of an issue on L2s (Arbitrum, Optimism) and BSC, but it’s worth calculating before you start.

How Yield Farming Returns Are Calculated

Two figures appear constantly: APY and APR. They’re not the same.

- APR (Annual Percentage Rate) is the simple interest return over a year — no compounding assumed. A pool showing 24% APR means you’d earn 24% if you deposited for exactly one year and never reinvested rewards.

- APY (Annual Percentage Yield) includes compounding. Earn 24% APR and reinvest daily, and your APY is approximately 27.1%. The compounding frequency is what creates the gap between the two figures.

Most DeFi interfaces display APY because it’s the bigger number. Here’s the catch: that assumes you’re auto-compounding, which many protocols don’t do automatically. If you claim rewards weekly and reinvest manually, your actual yield lands somewhere between APR and the displayed APY.

“If people tell me ‘You can get good yield by parking your coins here,’ my question always is, ‘Where does the yield come from?’ Who are the people on the other side of the transaction, who are paying the yield?” — Vitalik Buterin, co-founder of Ethereum

Math on Concrete Deposit

The math on a concrete deposit: put $5,000 USDC into a pool showing 10% APR. With daily compounding, you’d finish the year with approximately $5,526 — the displayed APY rounds to 10.52%. Without compounding (claiming monthly, leaving rewards idle), you’d end up at $5,500. The difference is small at moderate yield levels — it matters much more at 50%+ APR, where compounding frequency dramatically affects take-home returns.

One pattern experienced yield farmers track closely: protocols showing dramatically higher APY than competitors typically achieve it through heavy token emissions. When Compound launched the COMP governance token in 2020, the protocol reached nearly $500 million in staked value within a single trading day (Chainalysis, 2023). That yield was high because COMP was new and demand was speculative. Emissions-driven APY is a short-term opportunity, not a long-term income stream — and veteran farmers know to treat it as such.

The Bottom Line on Yield Farming

Yield farming works. The yields are real, the infrastructure is more battle-tested than it was in 2020, and stablecoin pools on Aave and Curve represent a genuine improvement over traditional savings rates. As of early 2026, you can earn 8-12% on USDC without taking on price volatility.

The part that trips people up is assuming that quoted APY translates directly to take-home return. Impermanent loss, gas fees, and token inflation all chip away at it. The farmers who do well are the ones who do the math before depositing, not after.

For most people starting out: stick to established protocols, focus on stablecoin pairs to sidestep impermanent loss, and treat governance token rewards as a bonus rather than the core thesis. Build from there.

To interact with these protocols, you’ll need a self-custody wallet. See our reviews of Trust Wallet and Coinbase Wallet to find one that fits your setup.

Frequently Asked Questions

1. Is yield farming safe?

Yield farming on established protocols like Aave and Curve carries lower risk than newer, unaudited platforms, but it’s never fully risk-free. Smart contract exploits, impermanent loss, and governance token devaluation are ongoing concerns. Stablecoin pools reduce price volatility exposure but don’t eliminate smart contract risk. Treat any amount deposited in DeFi as capital you could afford to lose.

2. What’s the minimum amount needed to start yield farming?

There’s no formal minimum, but Ethereum gas fees make small positions under $500-$1,000 economically inefficient. On Layer 2 networks like Arbitrum or Optimism, or on BSC via PancakeSwap, you can start with $100-$300 and keep gas fees proportional. Start small on a low-fee chain to learn the mechanics before committing larger capital to Ethereum mainnet pools.

3. What does APY mean in yield farming?

APY (Annual Percentage Yield) is the projected annual return assuming continuous compounding. DeFi interfaces typically display APY because it’s the larger figure — it assumes you reinvest rewards at every opportunity. If you’re claiming weekly and reinvesting manually, your actual return will be closer to the APR (Annual Percentage Rate) shown alongside it.

4. Can you lose money yield farming?

Yes. Impermanent loss, smart contract exploits, and governance token devaluation can all result in withdrawing less than you deposited. The riskiest positions are volatile token pairs on newer protocols running heavy token emissions. Stablecoin pairs on audited protocols like Curve are the lowest-risk entry point — not zero risk, but the closest to it in DeFi yield farming.

5. What is the difference between yield farming and liquidity mining?

Liquidity mining is a subset of yield farming. All liquidity mining involves providing liquidity to a pool and earning governance tokens as incentive. Yield farming is the broader category — it includes lending, borrowing, and multi-protocol strategies, not just liquidity provision. In practice the terms are used interchangeably, but “liquidity mining” specifically means earning protocol tokens for providing liquidity to an AMM or lending market.

This article is for educational purposes and does not constitute financial advice. Don’t put in money you need next month. DeFi carries real risks — smart contract exploits, protocol failures, and market volatility can all result in total loss of deposited funds.

Our Review Methodology

We evaluate each post based on thorough research, credibility of sources, accuracy of information, and relevance to our readers. Our editorial team follows strict guidelines to ensure all content meets high standards of quality.

Disclaimer

The content in this article is provided for informational purposes only and does not constitute financial, investment, or professional advice. Always do your own research before making any decisions.