The answer to ‘What is Defi?’ in simple terms is its full form: Decentralized Finance. To explain it further, your bank earns money on your deposits. It charges you fees to move your own money. If you want to send funds to someone in another country, you’ll face days of waiting and a percentage taken at each step. Decentralized finance (DeFi for short) was built on the premise that none of that has to be the default.

DeFi is a collection of financial services running on public blockchains, primarily Ethereum, using self-executing code called smart contracts. No banks, no brokers, no identity checks. By early 2026, total value locked across DeFi protocols sat between $130 and $140 billion (CoinLaw, February 2026). Not a fringe experiment.

Where Did DeFi Come From?

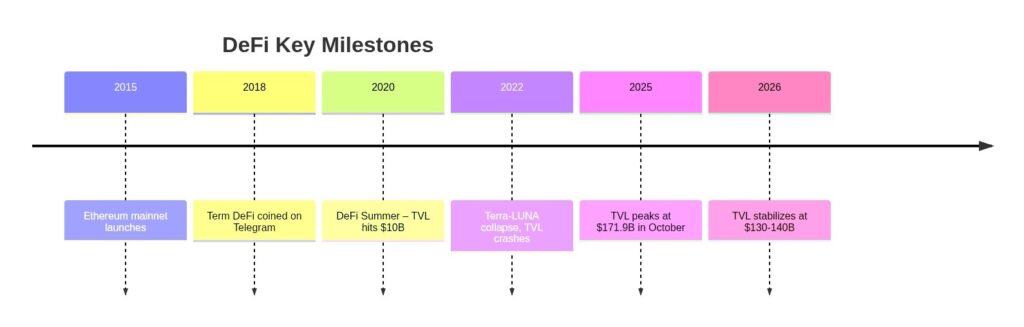

The 2008 financial crisis planted the seed. Ethereum’s arrival in 2015 gave developers the tools. The term “DeFi” itself was coined in August 2018 in a Telegram chat between Ethereum entrepreneurs and developers fitting for an ecosystem that built itself through community consensus before it built anything resembling institutional legitimacy.

- The first serious DeFi protocols arrived around 2019. MakerDAO let users lock ETH as collateral and mint DAI (a dollar-pegged stablecoin) effectively borrowing without a credit check. Compound introduced algorithmic interest rates set by supply and demand rather than a central bank. Uniswap built an exchange with no order book, no matching engine, just liquidity pools managed by code.

- Then came 2020, and what the community still calls “DeFi Summer.” Total value locked rocketed from under $1 billion in June to over $10 billion by September. The yields were eye-watering — 100%, 200%, sometimes more, generated by newly minted governance tokens handed out to early users.

- The 2022 Terra/LUNA collapse and the FTX implosion (technically CeFi, but it dragged everything with it) wiped out more than two-thirds of DeFi’s TVL. Recovery took three years. The $130B+ figure in early 2026 reflects a more cautious ecosystem, less yield-farming mania, more actual financial utility.

How Does DeFi Actually Work?

Everything runs on smart contracts, from code deployed to a blockchain that executes automatically when predetermined conditions are met. No human approves the transaction. No bank clears the funds. The contract either runs or it reverts; there’s no middle state where your funds are “under review.”

How Does it Work Using Smart Contracts?

Here’s a concrete example.

Want to borrow USDC using ETH as collateral? On Aave (one of the largest lending protocols, with roughly $27 billion in total deposits as of 2026), you’d connect your wallet, deposit ETH, and receive a borrowing allowance calculated automatically by the contract. Interest accrues block by block. Repay the loan and your collateral unlocks. Nobody reviewed your credit history. Nobody approved anything.

The overwhelming majority of DeFi activity runs on Ethereum, which commands roughly 68% of total DeFi TVL as of early 2026 (CoinLaw, 2026). Solana ($9.2 billion) and BNB Chain ($6.8 billion) make up significant chunks of the rest. Ethereum’s dominance isn’t accidental, it has the deepest developer ecosystem, the most audited contracts, and the longest track record of any programmable blockchain.

It’s worth noting that “permissionless” cuts both ways. Anyone can deploy a smart contract, which means bad actors can too.

What is DeFi vs What is CeFi: What’s the Real Difference?

CeFi or centralized finance is everything most crypto users start with. Coinbase, Binance, Kraken. The exchange controls your funds. They handle custody, order books, and KYC checks. When you deposit to Binance, Binance holds your crypto, not you. They can freeze accounts, restrict withdrawals, or go bankrupt.

DeFi flips the custody model entirely. Your private keys stay in your wallet. Protocols interact with your wallet directly, funds only moving when a transaction executes on-chain. When Celsius went bankrupt in 2022, users discovered that their deposited crypto was legally Celsius’s asset, not theirs, because that’s how custodial CeFi works. DeFi users with self-custody wallets weren’t affected by Celsius’s balance sheet at all.

“Self-custody isn’t a technicality — it’s the entire value proposition. The question ‘not your keys, not your coins’ stopped being a slogan the day Celsius filed for bankruptcy.” — Stani Kulechov, Founder, Aave

The trade-off is that there’s no customer support to call. No fraud protection. No FDIC insurance. Send funds to the wrong address or fall for a phishing site and nobody can reverse it.

KYC is the other real difference that can be cited while studying DeFi vs CeFi. CeFi platforms almost universally require identity verification, they’re legally obligated under AML regulations. I know for a fact that DeFi protocols generally can’t enforce KYC because there’s no gatekeeper to do it. Whether that’s a feature or a liability depends heavily on where you live and what you’re trying to do.

What Are the Main DeFi Protocols and Use Cases?

If I have to state in simple terms, “DeFi protocols” just means decentralized financial applications. There are hundreds of them, though they mostly fall into a few core categories.

- Decentralized exchanges (DEXs) let you swap tokens directly from your wallet, without depositing funds to any platform. Uniswap is the benchmark on Ethereum; Meteora and Raydium dominate on Solana. Weekly DEX trading volume across all chains topped $86 billion in early 2026, accounting for more than 21% of total crypto trading volume (CoinLaw, 2026). That’s not marginal volume anymore.

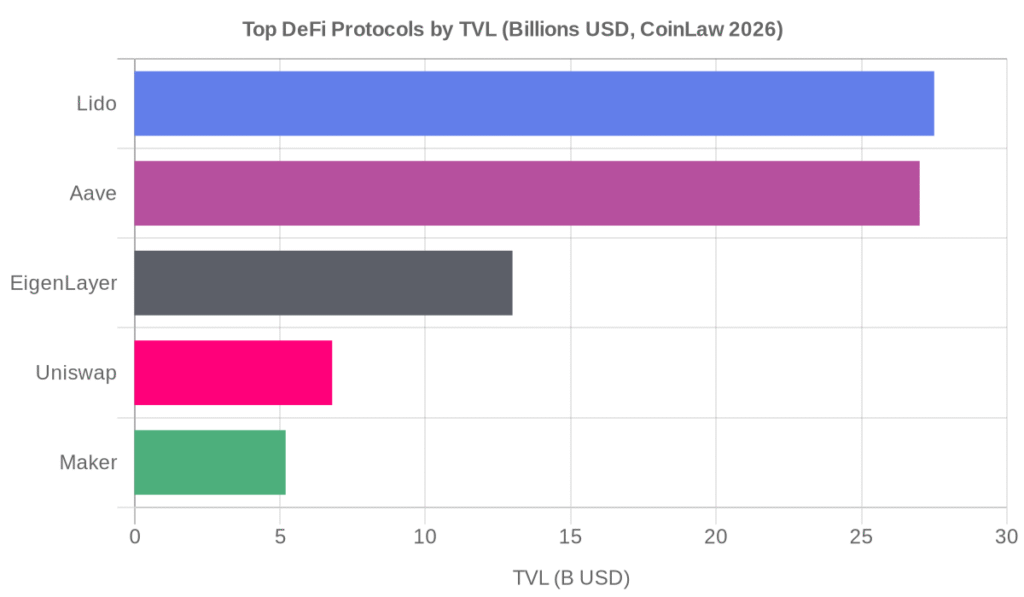

- Lending and borrowing protocols: Aave, Compound, Morpho let users deposit assets to earn yield or borrow against collateral. Rates are set algorithmically based on pool utilization, not board decisions. Aave has been operating since 2020 without a major smart contract exploit, which earns it a degree of “battle-tested” credibility in this space (though that word only goes so far, see the risks section).

- Liquid staking is where Lido has built the most dominant position in all of DeFi. Currently sitting at $27.5 billion in TVL, Lido lets you stake ETH and receive stETH in return — a liquid token representing your staked position that can still be deployed across other protocols. Genuinely useful product. It’s also attracted scrutiny for holding roughly 30% of all staked ETH, which raises questions about centralisation pressure on Ethereum’s consensus layer.

- Stablecoins underpin nearly everything. Their supply grew 49% in 2025 to approximately $300 billion outstanding (CoinLaw, 2026). USDC and USDT are the most used, both issued by centralised companies. DAI, issued by MakerDAO’s smart contracts and backed by on-chain collateral, is the most prominent decentralised alternative. If you’re interacting with DeFi regularly, you’ll use stablecoins constantly.

Is DeFi Safe? The Honest Risk Picture

Not entirely. That’s not a knock on DeFi specifically, no financial system is without risk but the risks here are different from what you’d encounter at a bank, and worth understanding specifically.

DeFi lost over $3.1 billion to security breaches in 2025 alone. Q1 2025 set a single-quarter record at $1.64 billion in losses (CoinLaw, 2026). The primary attack vectors are smart contract exploits (coding bugs identified by hackers before auditors find them), flash loan attacks (borrowing enormous sums within a single block to manipulate prices), and frontend phishing (fake websites that steal wallet permissions).

Smart contracts can’t be patched the way traditional software can. Once a contract is deployed, the code is fixed. Any bug discovered post-deployment is a live vulnerability until users migrate to a new version. Major protocols mitigate this through multiple security audits, bug bounty programs, and gradual liquidity limits on new contract versions. “Battle-tested” carries real meaning (Uniswap v2 has operated since 2020), but it doesn’t mean zero risk.

“Smart contract risk isn’t theoretical — it’s the defining risk of DeFi participation. A single unaudited function can drain a protocol with billions in TVL in minutes. Time-in-market without an exploit is the closest thing to a trust signal this industry has.” — Hayden Adams, Founder, Uniswap

Regulatory exposure is growing, particularly in the US. The SEC and CFTC have both claimed jurisdiction over DeFi activity, and protocols like Uniswap received SEC subpoenas (2024). In Europe, MiCA came into full effect in 2024 and is gradually clarifying what’s permissible — though “clarity” in crypto regulation is always relative.

And there’s just the complexity. DeFi interfaces are meaningfully better than they were in 2020, but they still assume a baseline of technical literacy that most people don’t have going in. Gas estimation, wallet approval hygiene, identifying legitimate contract addresses versus fake ones — these aren’t trivial skills when a mistake is permanent and unrecoverable.

Is DeFi Legal Where You Are?

Jurisdiction matters significantly. In the EU, MiCA (fully effective since 2024) provides a regulatory framework, though truly decentralized protocols sit in a grey zone. The US remains the most aggressive enforcement environment, the SEC and CFTC have both pursued DeFi-adjacent cases, and regulatory status for individual protocols is unsettled. In most Asian markets, including India, DeFi use is not explicitly prohibited, but tax treatment of on-chain activity is actively evolving. Always verify your local regulatory position before committing significant capital.

How Do You Start Using DeFi?

If you’re coming from a CeFi background (a Coinbase or Binance account) the main change is moving to a self-custody wallet. That’s where everything else follows from.

MetaMask is the most widely used wallet for Ethereum-based DeFi. It works as a browser extension and connects to essentially every major protocol. The key in all three cases: your seed phrase is your only recovery option, so store it offline, not in a cloud document.

Tradelize has a detailed MetaMask review if you want an in-depth look. For mobile use, Trust Wallet and Coinbase Wallet are both solid choices that support DeFi connections.

Once you have a wallet, fund it from an exchange. Buy ETH (or another asset), then withdraw it to your self-custody wallet address. Double-check the address before confirming. Triple-check it.

Connect to the protocol’s official website — uniswap.org, aave.com — and your wallet will prompt you to authorize a connection. You haven’t moved any funds yet at this point; you’ve just given the protocol permission to propose transactions for you to approve. Start with a small amount the first time. Even experienced DeFi users make expensive mistakes when trying something new.

Track your portfolio using the live cryptocurrency prices on Tradelize if you want a quick overview of what’s moving.

What Does DeFi Cost to Use?

Every transaction on Ethereum requires a gas fee paid in ETH. In 2026, simple token swaps on Ethereum mainnet typically cost $2–$8 during normal congestion(Solyzer, 2026); complex interactions like opening a lending position can run $15–$40. If those figures feel steep, Layer 2 networks like Arbitrum and Base run the same protocols for fractions of a cent. Most major DeFi protocols: Aave, Uniswap are fully accessible on L2s. Start there.

The Bottom Line on Decentralized Finance

DeFi gives anyone with a crypto wallet access to financial services that traditionally required a bank account, a broker, or a credit history. With $130–140 billion locked across protocols and more than 20 million unique users active in 2025, it’s well past the proof-of-concept stage. The real question isn’t whether DeFi works, it demonstrably does, but whether the risk trade-off makes sense for your situation.

For traders comfortable with self-custody and smart contract risk, DeFi opens access to yield opportunities, liquidity, and cross-border transfers that CeFi simply can’t match on speed or cost.

Frequently Asked Questions About DeFi

1. What does DeFi stand For?

DeFi stands for decentralized finance, a term coined in August 2018 by Ethereum developers to describe financial applications built on public blockchains without traditional intermediaries.

2. How is DeFi different from traditional finance?

Traditional finance relies on intermediaries — banks, brokers, exchanges — to verify, custody, and settle transactions. DeFi replaces them with smart contracts that execute automatically on-chain. Many traders find it faster and cheaper for specific use cases; international USDC transfers on Ethereum can settle in minutes for cents, compared to days and percentage fees for a bank wire.

3. What are examples of DeFi protocols?

The most widely used DeFi protocols include Lido (liquid staking, $27.5B TVL), Aave (lending and borrowing, ~$27B TVL), Uniswap (decentralized token exchange), MakerDAO (issuer of the DAI stablecoin), and EigenLayer (restaking, $13B TVL). These five protocols collectively represent the core of the current DeFi ecosystem, though there are hundreds of smaller ones across multiple chains.

4. Is DeFi a good investment?

DeFi protocols can generate yield through lending, staking, and liquidity provision. They’re also highly volatile, exposed to smart contract exploits, regulatory action, and crypto market corrections. We wouldn’t frame it as “investment” in the traditional sense — DeFi is financial infrastructure you either use or you don’t. Whether it makes sense for you depends on your goals and risk tolerance. Don’t put in money you’d need back next month.

5. Can DeFi protocols be hacked?

Yes. As covered in the risk section above, DeFi lost more than $3.1 billion to security breaches in 2025, with Q1 setting a single-quarter record. Smart contracts cannot be patched after deployment, making undiscovered bugs permanent vulnerabilities until users migrate to a newer contract version. Established protocols with multiple independent audits carry lower risk — but not zero.

Our Review Methodology

We evaluate each post based on thorough research, credibility of sources, accuracy of information, and relevance to our readers. Our editorial team follows strict guidelines to ensure all content meets high standards of quality.

Disclaimer

The content in this article is provided for informational purposes only and does not constitute financial, investment, or professional advice. Always do your own research before making any decisions.